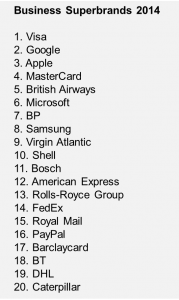

I’ve been having a quick look at the list of top 20 B2B brands compiled by Superbrands UK and published earlier in the week (see the full list of B2B superbrands here). Three things strike me as being really interesting:

Being a brand that is exclusively B2B isn’t enough

With the possible exception of Rolls Royce (where the aviation brand probably benefits from the association with the luxury car brand) none of the top 20 brands are exclusively B2B. They’re all present in both B2B and B2C and so perhaps should be viewed as B2B2C brands. Even a strongly ‘industrial’ brand like Caterpillar (number 20 in the current list) has become a B2B2C brand by virtue of its involvement in clothing and footwear.

With the possible exception of Rolls Royce (where the aviation brand probably benefits from the association with the luxury car brand) none of the top 20 brands are exclusively B2B. They’re all present in both B2B and B2C and so perhaps should be viewed as B2B2C brands. Even a strongly ‘industrial’ brand like Caterpillar (number 20 in the current list) has become a B2B2C brand by virtue of its involvement in clothing and footwear.

Maybe this B2B2C trend reflects the often forgotten fact that B2B decision makers are humans too. Experiences from their personal life will inevitably bleed into their business life.

Tech brands still dominate

Unsurprisingly tech brands still represent the largest single category within the top 20, not least because of the B2C overlap and their success in appealing to both B2B and B2C audiences. Some have fared better than others; Microsoft, Google and Apple have pretty much maintained their positions whereas Samsung is a clear winner, rising from 14 to 8. In sharp contrast IBM has dropped out of the top 20, having been sixth the year before. Interestingly, IBM is now positioned as a specialist B2B brand, having exited the PC market a few years ago. But as I suggested earlier, being an exclusively B2B brand may not be enough to command top 20 Superbrand status nowadays.

Financial services providers are being slowly forgiven for past misdemeanours

I accept that the likes of HSBC and Morgan Stanley don’t appear in the top 20; they probably should. But the rise of Visa (up from 4 to 1), Mastercard (10 to 4) and Amex (12 this year) is perhaps a sign of growing confidence in financial services brands, or at least those who are on the periphery. Perhaps surprisingly, UK perceptions of the Visa and Mastercard brands don’t seem to have been adversely affected by ongoing litigation in the US over excessive swipe charges.

What’s your take on the list? Please do share your comments below.